Pulse54: The 'Save Now, Buy Later' opportunity in Africa

Buy now, pay later has gradually become a mantra in global retailing, even in Africa. But now, plenty of shoppers are looking the other way—paying first and buying later.

Hey there! Welcome to another edition of Pulse54, your simple guide to African business, economy, finance, and technology.

This week, we explore an emerging trend ‘threatening’ to shake up the consumer finance landscape in Africa: Save Now, Buy Later.

But before we go on… If you’re not subscribed to this newsletter, hit the button below to sign up to get the next edition directly into your inbox!

Retail in Africa mostly happens in informal settings like street markets, small shops, and stalls.

These informal sellers, estimated at over 50 million across the continent, form the backbone of trade in many African countries.

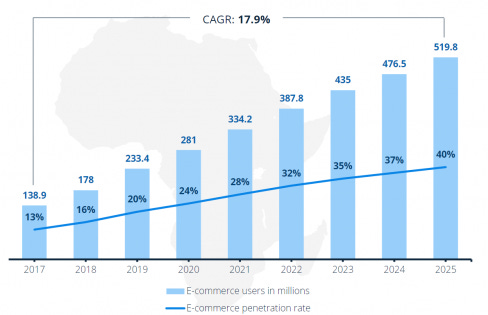

However, e-commerce is becoming more popular in the continent.

By 2025, Africa is expected to have more than 500 million online shoppers, a steady 17% compound annual growth rate (CAGR).

Even informal retailers are going digital, using online platforms and social media to sell their products, from car parts and used cars to fabrics and animal feed.

This shows that they are adapting to the increasing use of the internet by consumers in Africa.

But there’s still a buying-power problem in Africa that limits sales conversion for most of these vendors, despite reaching significantly more prospective customers.

In advanced economies, consumer credit solves this. However, both formal and informal African retailers struggle to offer this option.

Most of them work on a cash-only basis, making it hard for consumers to buy things if they don’t have all the money upfront.

It’s always been extremely tough for consumers in Africa to buy on credit, until the recent emergence of ‘buy now pay later’ (BNPL).

The rise (and fall?) of BNPL

In recent years, BNPL has become a popular way of funding purchases all around the world, including Africa.

The BNPL system usually works like this: you make a small down payment (around 20-25% of the item's price) and pass a credit check to get your item right away.

Then, you pay the rest in several equal installments over time.

Klarna is one of the leading global players in this market.

In Africa, BNPL has gained some ground, with companies like MNT-Halan, Lipa Later, Credpal, Carbon, and Payflex offering these services in different countries.

But there are now growing concerns about the sustainability of this model, with some companies losing a lot of money.

As losses tripled, Klarna’s valuation was slashed by 85% from ~$46bn in 2021 to ~$7bn in 2022.

Critics also argue that BNPL encourages impulsive spending and leads to debt problems.

While some BNPL services don't charge interest, many do, and late payments can come with hefty penalties.

Save now, buy later… to the rescue

In response to these concerns, a new approach to shopping is emerging, called 'save now, buy later' (SNBL).

SNBL platforms, also described as layaway or deferred payment services, allow you to reserve products and pay for them in installments over time, without the need for credit checks or high-interest loans.

Instead of getting the item right away, you pick a payment plan and make regular payments until the full amount is covered. You only receive the item once you've paid the full price.

This approach appeals to a broad consumer base, including those with limited access to traditional credit.

A growing global trend

One of the top global SNBL companies is Accrue Savings in the U.S., which partners with brands to integrate SNBL at checkout. They earn money through card fees and rewards from brands.

As you save, you earn cash rewards that lower the item's cost. If you change your mind, you can withdraw your funds without extra charges before completing the purchase.

SNBL encourages responsible spending and saving.

Other SNBL players include Monkee from Austria and Cashmere, which focuses on women's savings in the UK.

In India, companies like Tortoise, Hubble, and Multipl are leading the SNBL movement.

Tortoise offers BNPL solutions embedded in merchants' websites, similar to Accrue.

Hubble provides interest on savings and discounts for purchases made through its platform, while Multipl allows users to save directly with brands and earn cash rewards.

SNBL in Africa: An emerging sector with great potential

In Africa, SNBL is still new but promising.

Companies like FlexPay in Kenya, Tunzaa in Tanzania, LayUp in South Africa, and CDcare in Nigeria are pioneers.

FlexPay, particularly, helps customers save for purchases, earn rewards, and pay over time.

The startup aims to transform the financial landscape by combining technology, data insights, and partnerships with merchants to encourage responsible spending habits.

SNBL could help boost buying ability in Africa, a market where disposable incomes are low and inflation rates are skyrocketing.

Nearly half of the African population lives in poverty with only seven nations having a minimum wage of $200 or more.

For the majority, it’s below $100.

As a result, many African consumers cannot afford to pay outright for vital items like mobile phones or generators, which are crucial for their livelihoods and improving their quality of life.

More so, a large portion—over 66%—of the adult population is unbanked or underbanked.

For more context, more than 350 million adults in Africa live cash to cash and are without the safety net of a bank account, credit cards, or borrowing options.

With BNPL's shortcomings, SNBL holds great promise in Africa, offering a credit-free way to encourage responsible spending.

Platforms like FlexPay offer a credit-free solution that encourages responsible spending and empowers individuals to make purchases without accumulating debt.

For Africa’s 50 million+ SMEs, SNBL can attract new customers and boost sales. It's especially helpful for businesses selling big-ticket items like furniture or electronics.

Offering payment plans through SNBL platforms can expand their customer base and increase sales.

SNBL is a promising evolution of the BNPL model, offering affordability, scalability, and sustainability that are well-suited for the African market.

More importantly, the new model provides a solution for responsible shopping and access to credit.

The investment opportunity in SNBL

For investors, there are several reasons why the emerging SNBL platforms are an attractive prospect:

For investors, there are several reasons why SNBL platforms are an attractive prospect:

1. Market Growth: The adoption of SNBL platforms is on the rise globally, especially in regions with a growing middle class and increased access to the internet and smartphones. In emerging and developing markets, such as Africa, where credit card penetration is low and many consumers lack access to traditional banking, SNBL services fill a crucial gap.

2. Diverse Customer Base: SNBL platforms cater to a wide range of consumers, from those looking to purchase electronics, furniture, or even basic necessities. Additionally, SNBL allows for partnerships with retailers, enabling startups to earn revenue through fees and interest charges on installment payments. This diverse customer base ensures a steady flow of transactions and potential revenue streams.

3. Low Default Rates: Since SNBL platforms don't rely on traditional credit checks, the business model possesses little to no default risks. Also, cashbacks/rewards help in increasing customer satisfaction/loyalty especially if a user ends up buying from a particular merchant. This reduces the risk associated with investment in these platforms.

4. Scalability: The save-to-own approach rather than the credit model approach solves the problem of unaffordability in the vast African population, especially the average African who is averse to credit/debt. SNBL platforms could also cross into a wide range of verticals from insurance, and travel payments to bank/rental payments, and healthcare. With the right strategy and investment, players can scale rapidly, potentially reaching a much wider audience and increasing ROI exponentially.

The opportunity is glaring:

African consumers need better financing options if they are to become empowered to access purchases they previously could not afford.

Filling this gap could make a substantial difference in capturing more African consumers, and broadly, contributing to financial inclusion and economic development across the continent.

Would you like to learn more about exciting investment opportunities in the emerging "Save Now, Buy Later" space? Express your interest today by filling out our form below and be part of the journey toward shaping the future of Africa’s consumer finance landscape!

Disclaimer: This article is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation for any security; nor does it constitute an offer to provide investment advisory or other services. Interested parties should conduct their own due diligence and seek independent investment advice before making any investment decisions.

Pulse54 is sent twice a month. Think your friend or colleague should know about us? Forward this newsletter to them. They can also sign up here.

You can also download the Daba app to get daily bite-sized insights into African economies, industry and country reports, and access investment opportunities.

That's all for this week.

Until next time!